Wearables had a varied year in 2015, with a lot of hype and a few big winners streaking ahead of the field, leaving plenty of also-rans struggling to stand out.

It’s fair to say that the entire category is yet to prove whether it offers lasting utility or mere faddish novelty. The success of the smartphone is such than any supplementary technology inevitably lives in its shadow — and wearables are all about offering some kind of add-on functionality. Mobile undoubtedly still wears tech’s crown, and will do for the foreseeable future.

Apple arrives

The wearable category climax — at least, from a consumer point of view — was the much anticipated launch of Cupertino’s first foray into wrist-mounted gadgetry. Although confirmed by the company in fall last year, Apple Watches only started arriving in the hands of pre-orderers this April.

Long-standing rumors that Apple was making a wearable arguably fired up and fueled the entire category in earlier years, with rivals scrambling to get their own wrist-based gizmosinto the market in the hopes of making a mark before Apple could.

But with Apple finally having its watch in play the frenzy to be first evaporated — and with it a little of the fire that was fueling early wearable developments. That’s not a bad thing, given that hasty attempts to out-do a device that doesn’t even exist yet are hardly a perfect recipe for thoughtful product design.

So what of Apple’s wearable? The jury is still out on its utility — reviewers generally failed to articulate what exactly the gizmo is for. And as for sales, Apple doesn’t break out Watch sales, but analyst Canalys estimates it sold some 7 million over the first two initial quarters on sale. Not bad for a device without a clear proposition. Those quarters were not holiday season, either. So sales are bound to get a further festive bump through the end of the year.

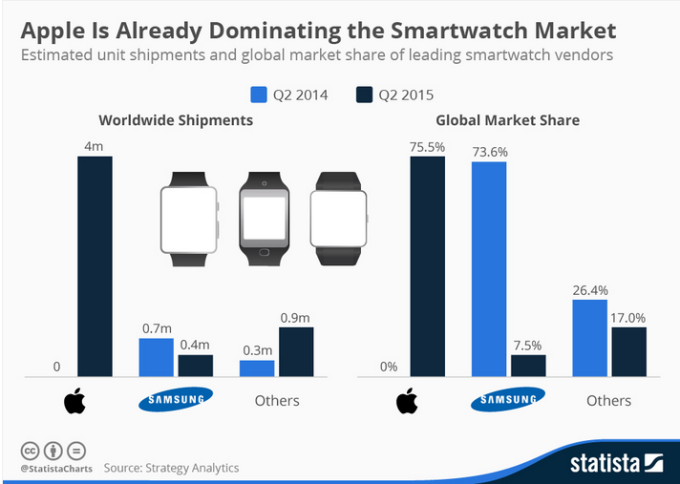

For some comparative context sales of Samsung’s Galaxy Gear smartwatches (pictured below), which have been in the market since debuting in 2013, apparently totaled some 1.2 million in 2014, according to analyst statista estimates.

Quite how big and festive the Apple Watch festive bump ends up being remains to be seen. But it seems likely that 2015 ended with Apple in second place in the wearables category, behind fitness tracker maker Fitbit — which sold 4.8 million devices between July and September.

Apple vs Fitbit is something of an apples to oranges comparison, given the price-differential between the Apple Watch and Fitbit’s range of trackers — the latter’s wearables start at less than $50 for its Zip-clip step-tracker and rise to $250 for its flagship Surge smartwatch. And the fact the Apple Watch offers fitness tracking as one of myriad possible functions, rather than as its raison d’être — as Fitbit does.

When it comes to just smartwatches, Apple appears to have taken a clear lead. By this summer statista concluded the company was already dominating smartwatches, despite rivals like Samsung having a category headstart of well over a year.

One notable Apple Watch development as the year went on was a collaboration with luxury accessories brand Hermès. A Hermès Apple Watch leather strap launched in the fall. The odd pairing of an old world luxury brand with newfangled fashion tech underlines how difficult the wearables category is when it comes to satisfying consumers’ personal tastes. The Apple brand may be premium in tech terms but it’s still the new kid on the block in the long-lived world of luxury fashion.

What will be key in 2016 is how sustainable Apple Watch sales prove to be — as the novelty of a new Apple device wears off leaving the utility of the watch to prove itself by convincing buyers they really do need an expensive supplementary gizmo on their wrist. TechCrunch’s own Josh Constine remains to be convinced.

Elsewhere in the smartphone space, LG canceled its latest smartwatch model after less than a week on sale, citing hardware problems. And an embattled HTC, still sweating to turn around its mobile fortunes, delayed the release of a planned co-branded fitness band with Under Armour. The mobile maker has so far stayed away from smartwatches — although rumors are it will rectify that early in 2016.

Misfit sells

Meanwhile in 2015, fitness wearable maker Misfit sold to fashion accessory and watch maker Fossil for $260 million — not an amazing return for investors who had put $64.4 million into the company, across three rounds of funding, since it was founded in 2011. Although, from Misfit’s point of view, it’s a story of a series of successful investment decisions, not least the$20k the startup spent on its crowdfunding pitch video which turned into almost $850k in crowdfunds raised via Indiegogo — and eventually that $260M exit to Fossil.

The sight of a smaller wearable maker being folded into an established watch brand is interesting from the point of view of determining which is more important for wearables: fashion or technology? Fossil said it will be integrating Misfit tech into its existing watch brands. So it’s evidently confident in its design smarts. But reckons it’s just a case of needing to add a little tech to stay competitive. Time will tell on that one.

Fitbit IPOs

Another wearables high point this year was Fitbit’s IPO in June, which saw the values of its shares spiking by as much as 50 per cent as it begun trading. The company pulled in nearly $740 million from the IPO. Its shares have continued to hold their value.

Speaking at TechCrunch Disrupt SF in September, Fitbit CEO and co-founder James Park described the health and fitness category as “a pretty large and diverse opportunity”, noting that consumers spend over $200 billion on related products and services — and arguing that Fitbit’s kit does not significantly overlap with Apple’s wearables play here. The company certainly offers a far larger range of wearables at this point, and all its devices undercut the Apple Watch on price.

“There’s going to be a lot of different companies that win in different bits of this market,” Park argued. “For us and Apple, we don’t see ourselves as directly competitive today. And the numbers show it. Year over year our revenue tripled towards $400 million last quarter. The guidance that we gave analysts for our last earnings call was $1.7 billion in revenue this year, so we’re doing incredibly well. And I think consumers like the fact that we’re really focused on the category.”

Being tightly focused on fitness also seems to be enabling Fitbit’s brand to transcend the fashion issue which continues to hamper other smartwatch and wearable makers. Point is, if you’re intending to sweat on something you’re going to be less fussed about how fashionable that something looks.

Sweating toil in the wearables pack

While investors rewarded Fitbit by keeping its share price buoyant, other fitness-focused wearable players weathered tougher times in 2015.

Early in the year Jawbone, maker of the UP fitness trackers, continued to be beset with manufacturing woes delaying its latest wearable, the UP3 (pictured below). There was in fact no IPO for the company in 2015 — instead it got a $300 million convertible loan, and had to shrink operations, including making staff cuts, going on to slash 15 per cent of its workforce in November. Ongoing legal clashes with Fitbit also piled more distractions onto its plate.

Rumors of tough times also dogged early wearable darling, Pebble, which revealed early in the year that it had shipped 1 million devices cumulatively, over some three years in the game. Years when it was not having to compete directly with Apple, of course. How Pebble is responding to competition from the Apple Watch was a question continually — and inevitably — fired at CEO Eric Migicovsky this year.

He claimed the company is seeing “no material impact” from the arrival of the Apple Watch, telling CNBC in November: “They are very focused on being the Rolex or the (Tag Heuer) of smartwatches. On the other hand I think we are trying to be the Swatch of smartwatches. We are building something that’s fun, a little bit more colourful. It’s affordable. At the core, it’s just a different type of watch.”

The notifications wristwear-maker kicked things up a gear on the design front this fall, announcing its first round-faced smartwatch — the Pebble Time Round (pictured below) — priced between $249 and $299. The round design entails an unfortunate compromise on the battery life front, shrinking the typical five or six days’ of juice down to just two – and thereby reducing one big differentiating advantage vs the Apple Watch.

Price wise Pebble’s flagship remains cheaper than the entry level Apple Watch ($350), however Best Buy in the US discounted the Apple Watch by $100 at the back end of the year – which underlines how Apple’s pricing is hardly well characterized as akin to Rolex levels of luxury. There’s actually only a small premium standing between Apple kit and Pebble’s flagships.

Apple is also rumored to be planning another Watch event for March 2016. It would not be unusual for Cupertino to reduce the price of an older gen device as it launches a new version so that differentiating price margin between the Apple Watch and the rest of the smartwatch field may well shrink further.

Whatever happens in the short term, there’s little doubt Pebble is sitting in a tough spot — squeezed between Apple at the high end and an ever growing sea of mid range smartwatches and notification gizmos all vying for consumer attention.

Xiaomi undercuts

Talking of budget wearables, Chinese upstart Xiaomi got into the space in mid 2014 with a $13 waterproof fitness band, which tracks steps, activity, sleep and more, and has a month-long battery life so is designed to be worn daily, continuing the company’s philosophy of disrupting the competition on price.

That hyper budget pricing strategy saw Xiaomi step up its share of the wearables market this year, with analyst IDC estimating it had taken a quarter of the market by Q1 2015, shipping 2.8 million of its Mi Bands (vs 3.9 million Fitbits). That placed Xiaomi second globally by mid 2015, when it opened up Mi Band sales to the U.S. and Europe. And third by Q2, behind Fitbit and Apple. Such is the scale of the Chinese market.

Xiaomi added a second wearable device, the Mi Band Pulse (pictured above), in November, also priced very aggressively, at around $15. Rumors that the company would branch out into the smartwatch space have yet to come true but do seem likely given its existing playbook of offering a comprehensive portfolio of device types to compete with all the products sold by rivals.

That said, fashion is a fickle creature. And without a clearly articulated purpose for smartwatches how they look is pretty important — so a budget Xiaomi smartwatch isn’t necessarily going to be too exciting from a consumer point of view. Unless it’s offering some super compelling function.

Undercutting the competition on price at least looks set to sustain Xiaomi as a significant player in fitness wearables, where looks are less important — provided its strategy of wafer-thin profits is sustainable. And provided it can see off growing competition from other fast-following Chinese makers also intent on earning a place on consumers’ wrists.

Rings and things

Elsewhere, investors made a few bets on some fashion-focused wearables in 2015, with so-called ‘smart jewelry’ startups pulling in some dollars.

At the start of the year bothRingly and Cuff (the latter pictured, right) raised almost identical Series A rounds in the $5M range. The two startups play in the screenless notifications space, and also — in Cuff’s case — have plans to integrate fitness tracking into fine jewelry too in future.

At the start of the year bothRingly and Cuff (the latter pictured, right) raised almost identical Series A rounds in the $5M range. The two startups play in the screenless notifications space, and also — in Cuff’s case — have plans to integrate fitness tracking into fine jewelry too in future.

Vinaya, which detailed its $3M seed this fall, is another startup focused on putting tech inside fine jewelry, embedding notifications systems into designer wearables. The general thinking that links all these players is the idea that (some) women want an alternative way to be notified of incoming messages — i.e. without having to keep checking their smartphone.

With fashion being such a multifaceted animal there is room for plenty of niche fashion-tech plays to offer an alternative to people who wouldn’t be caught dead wearing an ugly piece of plastic but might be persuaded to slip on something that can pass as costume jewelry. But whether any of these businesses can scale into something more significant than a niche player is a big question mark.

The challenge they are setting themselves is twofold: not just producing slick and useful tech features but embedding those in a designer wrapper that looks good enough to compete with the likes of the Apple Watch and luxury/premium fashion brands who are also targeting this demographic. A tricky balancing act to pull off then.

Headsets get hyped

Meanwhile, another kind of wearable — the virtual reality headset — was making waves in 2015. Albeit, mostly hype waves. Or else the kind that make people feel queasy.

Consumer demand for virtual reality has yet to be tested but we sure heard a lot of hype about VR this year with tech companies lining up to pour dollars into the idea that The Next Big Thing will be a vision-altering headset. Not that we haven’t heard that line before…

Even beleaguered HTC is betting on the VR space, albeit in partnership with games maker Valve. The pair announced a collaboration this Spring but the HTC/Valve Vive isn’t shipping in any quantities til April next year.

Also still in development stasis: the now Facebook-owned Oculus Rift. The $2BN acquisition closed in July 2014 but the headset isn’t due to ship til Q1 2016. But you’d hardly know that judging by the stream of Rift-based PR being issued this year as the company attempted to fire up developers to build ‘experiences’ for its forthcoming headset, while also priming gamers to be ready to slip on a face computer and gawp open-mouthed into other worlds.

The start of 2015 also saw Microsoft get in on the virtual action, when it showed off an augmented reality headset it’s building called Hololens. Not full VR but the blended compromise that is augmented reality, which mixes digital content into a real world perspective. Microsoft demoed its headset being used to play games like Minecraft and for more practical stuff like doing a spot of DIY plumbing.

In less positive signs for Redmond’s AR vision, by the end of the year it was laying off Hololens staff without explaining why. Rumors suggest it isn’t happy with the tech’s development. The dev version of Hololens is not due til Q1 2016 but given the rethinking Redmond is already doing it seems prudent to expect some delays.

The biggest winner of the still untested (and largely unformed) VR/AR space in 2015 was perhaps Magic Leap, a stealthy startup that’s building some sort of AR headset. Details of what exactly it’s making are scant but it’s attracted some big name investors, including Google. And has a serious war chest – of more than $1 billion — at its disposal.

In December it emerged Magic Leap had scored a $827M Series C funding round so while the startup still can’t bank on reliable consumer demand for vision-disrupting wearables, it can at least say its vision has convinced investors to make some very big bets indeed.

AR goes to work

For all Magic Leap’s flashy, consumer-focused demos — such as these videos of zombies roaming an office — the more mundane reality of augmented reality might actually be something early mover Google Glass is now apparently focused on.

While Glass never earned more than mockery from the mainstream consumer, it appears to be carving out a niche for itself in the enterprise space, for things like warehousing inventory or security tasks. And while the year began with Google withdrawing Glass from consumer sale, it ended with a report detailing new designs for a more robust enterprise version of the wearable – underscoring that Google isn’t giving up on Glass entirely.

Wearing an AR headset for work neatly circumvents the stigma associated with the general public rocking a face computer when mingling with their fellow humans. And while pure VR can shut itself away from public ridicule in a private room, AR’s pitch tends to involve claims of more general utility because of the blended view it offers. (For instance, discussing Magic Leap this March, Google’s Sundar Pichai, who sits on the company board, said Google sees broad use-cases for the augmented reality tech – i.e. not just gaming.)

However no-one wants to be walking around alienating strangers by drawing unwanted attention to a gizmo sitting on their nose. So unless Magic Leap’s technology is indistinguishable from a pair of glasses it’s going to have a tough time blending in in a way that’s socially acceptable.

And even then, people don’t want to wear the same pair of glasses. Typically the first decision a glasses-buyer makes is about the style of the frames they reckon suits them. It’s a highly personal fashion purchase. So for Magic Leap to really fly it would need to be a technology that can be invisibly fitted to third party glasses frames. No pressure then.

Seen from that angle, mid to low range VR headsets like the super budget Google Cardboard, or Samsung’s $100 Gear VR, which went on sale this November — which can offer gamers a novel diversion that doesn’t break the bank, being as it utilizes their existing smartphone hardware — have perhaps the most realistic chance of making a sizable impression with consumers. Samsung certainly made a lot of noise about the Gear VR leading up to its launch. And scored a bespoke game designed for it by London based design studio ustwo — of Monument Valley fame.

As things stand right now, the most visible impact of VR remains the distinctive, slack-jawed expression on the faces of people caught peering into ‘The Future’…

Source: http://techcrunch.com/